Abstract:

Traditionally, accounting makes the apportionment of indirect costs in the full cycle beef cattle activity based on the unit cost per animal (head). By this criterion, the cost value attributed to a calf is the same for an adult animal (cow), which suggests not be most appropriate criterion. The use of agricultural inputs, food consumption and the purchase and sale of animals occur according to body weight. Provide an apportionment criterion that allows distribution of the production costs to the herd taking into account the body weight would be the most appropriate. Proposing the apportionment of the overhead costs of the full cycle beef cattle activity based on the animal unit (AU) is the objective of this study, since it allows classifying beef cattle of different ages and sex in the same evaluation basis. The results confirmed differences among the apportionment criteria, pointing out that the animal unit is the most appropriate for apportioning costs in full cycle beef cattle

Key-words:

Beef cattle accounting; Indirect costs; Sharing cost.

Thumbnail

Thumbnail

Thumbnail

Thumbnail

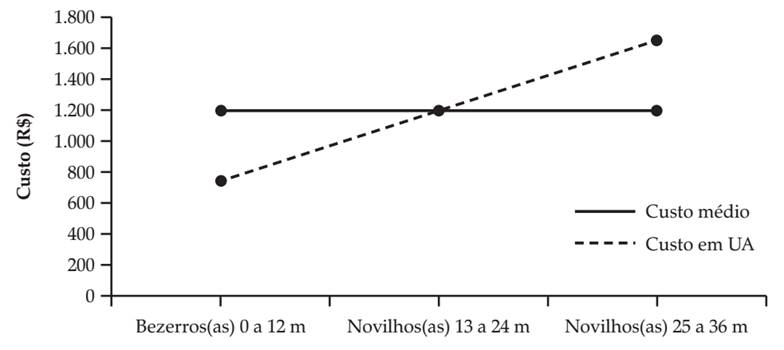

Fonte: Elaboración propia.

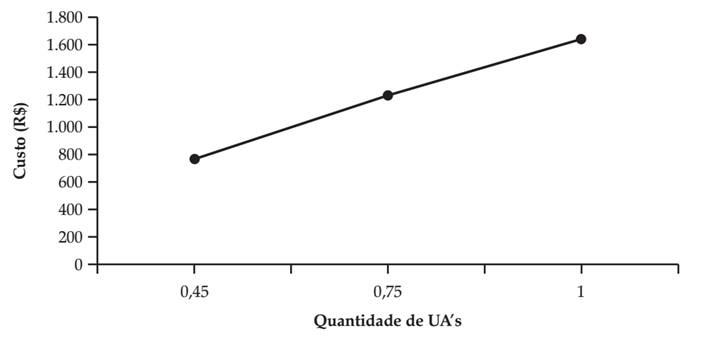

Fonte: Elaboración propia.

Fonte: Elaboración propia.

Fonte: Elaboración propia.